Time series#

Co-author

Prerequisites

Outcomes

Know how pandas handles dates

Understand how to parse strings into

datetimeobjectsKnow how to write dates as custom formatted strings

Be able to access day, month, year, etc. for a

DateTimeIndexand a column withdtypedatetimeUnderstand both rolling and re-sampling operations and the difference between the two

Data

Bitcoin to USD exchange rates from March 2014 to the present

# Uncomment following line to install on colab

#! pip install

import os

# see section on API keys at end of lecture!

import pandas as pd

import matplotlib.pyplot as plt

import nasdaqdatalink as ndl

ndl.ApiConfig.api_key = os.environ.get("NASDAQ_DATA_LINK_API_KEY", "jEKP58z7JaX6utPkkpEp")

start_date = "2014-05-01"

%matplotlib inline

Intro#

pandas has extensive support for handling dates and times.

We will loosely refer to data with date or time information as time series data.

In this lecture, we will cover the most useful parts of pandas’ time series functionality.

Among these topics are:

Parsing strings as dates

Writing

datetimeobjects as strings (inverse operation of previous point)Extracting data from a DataFrame or Series with date information in the index

Shifting data through time (taking leads or lags)

Re-sampling data to a different frequency and rolling operations

However, even more than with previous topics, we will skip a lot of the functionality pandas offers, and we urge you to refer to the official documentation for more information.

Parsing Strings as Dates#

When working with time series data, we almost always receive the data with dates encoded as strings.

Hopefully, the date strings follow a structured format or pattern.

One common pattern is YYYY-MM-DD: 4 numbers for the year, 2 for the

month, and 2 for the day with each section separated by a -.

For example, we write Christmas day 2017 in this format as

christmas_str = "2017-12-25"

To convert a string into a time-aware object, we use the

pd.to_datetime function.

christmas = pd.to_datetime(christmas_str)

print("The type of christmas is", type(christmas))

christmas

The type of christmas is <class 'pandas._libs.tslibs.timestamps.Timestamp'>

Timestamp('2017-12-25 00:00:00')

The pd.to_datetime function is pretty smart at guessing the format

of the date…

for date in ["December 25, 2017", "Dec. 25, 2017",

"Monday, Dec. 25, 2017", "25 Dec. 2017", "25th Dec. 2017"]:

print("pandas interprets {} as {}".format(date, pd.to_datetime(date)))

pandas interprets December 25, 2017 as 2017-12-25 00:00:00

pandas interprets Dec. 25, 2017 as 2017-12-25 00:00:00

pandas interprets Monday, Dec. 25, 2017 as 2017-12-25 00:00:00

pandas interprets 25 Dec. 2017 as 2017-12-25 00:00:00

pandas interprets 25th Dec. 2017 as 2017-12-25 00:00:00

However, sometimes we will need to give pandas a hint.

For example, that same time (midnight on Christmas) would be reported on an Amazon transaction report as

christmas_amzn = "2017-12-25T00:00:00+ 00 :00"

If we try to pass this to pd.to_datetime, it will fail.

pd.to_datetime(christmas_amzn)

---------------------------------------------------------------------------

DateParseError Traceback (most recent call last)

Cell In[6], line 1

----> 1 pd.to_datetime(christmas_amzn)

File ~/miniconda3/envs/lecture-datascience/lib/python3.12/site-packages/pandas/core/tools/datetimes.py:1101, in to_datetime(arg, errors, dayfirst, yearfirst, utc, format, exact, unit, infer_datetime_format, origin, cache)

1099 result = convert_listlike(argc, format)

1100 else:

-> 1101 result = convert_listlike(np.array([arg]), format)[0]

1102 if isinstance(arg, bool) and isinstance(result, np.bool_):

1103 result = bool(result) # TODO: avoid this kludge.

File ~/miniconda3/envs/lecture-datascience/lib/python3.12/site-packages/pandas/core/tools/datetimes.py:435, in _convert_listlike_datetimes(arg, format, name, utc, unit, errors, dayfirst, yearfirst, exact)

432 if format is not None and format != "mixed":

433 return _array_strptime_with_fallback(arg, name, utc, format, exact, errors)

--> 435 result, tz_parsed = objects_to_datetime64(

436 arg,

437 dayfirst=dayfirst,

438 yearfirst=yearfirst,

439 utc=utc,

440 errors=errors,

441 allow_object=True,

442 )

444 if tz_parsed is not None:

445 # We can take a shortcut since the datetime64 numpy array

446 # is in UTC

447 out_unit = np.datetime_data(result.dtype)[0]

File ~/miniconda3/envs/lecture-datascience/lib/python3.12/site-packages/pandas/core/arrays/datetimes.py:2398, in objects_to_datetime64(data, dayfirst, yearfirst, utc, errors, allow_object, out_unit)

2395 # if str-dtype, convert

2396 data = np.asarray(data, dtype=np.object_)

-> 2398 result, tz_parsed = tslib.array_to_datetime(

2399 data,

2400 errors=errors,

2401 utc=utc,

2402 dayfirst=dayfirst,

2403 yearfirst=yearfirst,

2404 creso=abbrev_to_npy_unit(out_unit),

2405 )

2407 if tz_parsed is not None:

2408 # We can take a shortcut since the datetime64 numpy array

2409 # is in UTC

2410 return result, tz_parsed

File tslib.pyx:414, in pandas._libs.tslib.array_to_datetime()

File tslib.pyx:596, in pandas._libs.tslib.array_to_datetime()

File tslib.pyx:553, in pandas._libs.tslib.array_to_datetime()

File conversion.pyx:641, in pandas._libs.tslibs.conversion.convert_str_to_tsobject()

File parsing.pyx:336, in pandas._libs.tslibs.parsing.parse_datetime_string()

File parsing.pyx:666, in pandas._libs.tslibs.parsing.dateutil_parse()

DateParseError: Unknown datetime string format, unable to parse: 2017-12-25T00:00:00+ 00 :00, at position 0

To parse a date with this format, we need to specify the format

argument for pd.to_datetime.

amzn_strftime = "%Y-%m-%dT%H:%M:%S+ 00 :00"

pd.to_datetime(christmas_amzn, format=amzn_strftime)

Timestamp('2017-12-25 00:00:00')

Can you guess what amzn_strftime represents?

Let’s take a closer look at amzn_strftime and christmas_amzn.

print(amzn_strftime)

print(christmas_amzn)

%Y-%m-%dT%H:%M:%S+ 00 :00

2017-12-25T00:00:00+ 00 :00

Notice that both of the strings have a similar form, but that instead of actual numerical values, amzn_strftime has placeholders.

Specifically, anywhere the % shows up is a signal to the pd.to_datetime

function that it is where relevant information is stored.

For example, the %Y is a stand-in for a four digit year, %m is

for 2 a digit month, and so on…

The official Python

documentation contains a complete list of possible %something patterns that are accepted

in the format argument.

Exercise

See exercise 1 in the exercise list.

Multiple Dates#

If we have dates in a Series (e.g. column of DataFrame) or a list, we

can pass the entire collection to pd.to_datetime and get a

collection of dates back.

We’ll just show an example of that here as the mechanics are the same as a single date.

pd.to_datetime(["2017-12-25", "2017-12-31"])

DatetimeIndex(['2017-12-25', '2017-12-31'], dtype='datetime64[ns]', freq=None)

Date Formatting#

We can use the %pattern format to have pandas write datetime

objects as specially formatted strings using the strftime (string

format time) method.

For example,

christmas.strftime("We love %A %B %d (also written %c)")

'We love Monday December 25 (also written Mon Dec 25 00:00:00 2017)'

Exercise

See exercise 2 in the exercise list.

Extracting Data#

When the index of a DataFrame has date information and pandas

recognizes the values as datetime values, we can leverage some

convenient indexing features for extracting data.

The flexibility of these features is best understood through example, so let’s load up some data and take a look.

btc_usd_long = ndl.get_table("QDL/BCHAIN", date = { 'gte': '2009-12-25', 'lte': '2019-01-01' }, code = ["MKPRU", "MKTCP", "ETRVU"])

btc_usd_long.info()

btc_usd_long.head()

<class 'pandas.core.frame.DataFrame'>

RangeIndex: 9885 entries, 0 to 9884

Data columns (total 3 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 code 9885 non-null object

1 date 9885 non-null datetime64[ns]

2 value 9885 non-null float64

dtypes: datetime64[ns](1), float64(1), object(1)

memory usage: 231.8+ KB

| code | date | value | |

|---|---|---|---|

| None | |||

| 0 | MKTCP | 2019-01-01 | 6.550566e+10 |

| 1 | MKTCP | 2018-12-31 | 6.638886e+10 |

| 2 | MKTCP | 2018-12-30 | 6.689905e+10 |

| 3 | MKTCP | 2018-12-29 | 6.827565e+10 |

| 4 | MKTCP | 2018-12-28 | 6.709189e+10 |

Here, we have the Bitcoin (BTC) to US dollar (USD) exchange rate from 2009 until today, as well as other variables relevant to the Bitcoin ecosystem, in long (“melted”) form.

print(btc_usd_long.code.unique())

btc_usd_long.dtypes

['MKTCP' 'MKPRU' 'ETRVU']

code object

date datetime64[ns]

value float64

dtype: object

Notice that the type of date is datetime. We would like this to be the index, and we want to drop the long form. We also selected only a couple of columns of interest, but the dataset has a lot more options. (The column descriptions can be found here). We chose Market Price (in USD) (MKPRU), Total Market Cap (MKTCP), and Estimated Transaction Volume in USD (ETRVU).

btc_usd = btc_usd_long.pivot_table(index='date', columns='code', values='value')

btc_usd.head()

| code | ETRVU | MKPRU | MKTCP |

|---|---|---|---|

| date | |||

| 2009-12-25 | 0.0 | 0.0 | 0.0 |

| 2009-12-26 | 0.0 | 0.0 | 0.0 |

| 2009-12-27 | 0.0 | 0.0 | 0.0 |

| 2009-12-28 | 0.0 | 0.0 | 0.0 |

| 2009-12-29 | 0.0 | 0.0 | 0.0 |

Now that we have a datetime index, it enables things like…

Extracting all data for the year 2015 by passing "2015" to .loc.

btc_usd.loc["2015"]

| code | ETRVU | MKPRU | MKTCP |

|---|---|---|---|

| date | |||

| 2015-01-01 | 2.831524e+07 | 316.15 | 4.388454e+09 |

| 2015-01-02 | 5.458287e+07 | 314.81 | 4.136728e+09 |

| 2015-01-03 | 9.035606e+07 | 270.93 | 3.708212e+09 |

| 2015-01-04 | 6.263383e+07 | 276.80 | 3.901250e+09 |

| 2015-01-05 | 5.647246e+07 | 263.17 | 3.790804e+09 |

| ... | ... | ... | ... |

| 2015-12-27 | 7.700877e+07 | 418.46 | 6.420190e+09 |

| 2015-12-28 | 1.057652e+08 | 422.42 | 6.366855e+09 |

| 2015-12-29 | 1.158679e+08 | 431.13 | 6.475864e+09 |

| 2015-12-30 | 9.992696e+07 | 428.00 | 6.386794e+09 |

| 2015-12-31 | 7.566080e+07 | 428.23 | 6.452379e+09 |

365 rows × 3 columns

We can also narrow down to specific months.

# By month's name

btc_usd.loc["August 2017"]

| code | ETRVU | MKPRU | MKTCP |

|---|---|---|---|

| date | |||

| 2017-08-01 | 1.369196e+09 | 2862.9000 | 4.550093e+10 |

| 2017-08-02 | 1.424506e+09 | 2693.6340 | 4.440385e+10 |

| 2017-08-03 | 9.709563e+08 | 2794.1177 | 4.606512e+10 |

| 2017-08-04 | 1.196485e+09 | 2790.0000 | 4.631086e+10 |

| 2017-08-05 | 9.791541e+08 | 3218.1150 | 5.306965e+10 |

| 2017-08-06 | 1.044204e+09 | 3252.5625 | 5.364342e+10 |

| 2017-08-07 | 1.385571e+09 | 3210.2000 | 5.319216e+10 |

| 2017-08-08 | 1.230026e+09 | 3457.3743 | 5.703501e+10 |

| 2017-08-09 | 8.071196e+08 | 3357.3263 | 5.526816e+10 |

| 2017-08-10 | 9.631284e+08 | 3340.2800 | 5.650275e+10 |

| 2017-08-11 | 9.856015e+08 | 3632.5067 | 5.994299e+10 |

| 2017-08-12 | 8.706294e+08 | 3852.8029 | 6.358478e+10 |

| 2017-08-13 | 9.264450e+08 | 3868.5200 | 6.693611e+10 |

| 2017-08-14 | 8.666749e+08 | 4282.9920 | 7.069930e+10 |

| 2017-08-15 | 1.206088e+09 | 4217.0283 | 6.961845e+10 |

| 2017-08-16 | 9.825228e+08 | 4179.9700 | 6.764231e+10 |

| 2017-08-17 | 1.362841e+09 | 4328.7257 | 7.147917e+10 |

| 2017-08-18 | 1.137242e+09 | 4130.4401 | 6.821262e+10 |

| 2017-08-19 | 1.323689e+09 | 4104.7100 | 6.812422e+10 |

| 2017-08-20 | 7.589911e+08 | 4157.9580 | 6.868167e+10 |

| 2017-08-21 | 8.194572e+08 | 4043.7220 | 6.680052e+10 |

| 2017-08-22 | 8.814776e+08 | 3986.2800 | 6.755553e+10 |

| 2017-08-23 | 1.053264e+09 | 4174.9500 | 6.898129e+10 |

| 2017-08-24 | 7.560436e+08 | 4340.3167 | 7.171907e+10 |

| 2017-08-25 | 7.651743e+08 | 4331.7700 | 7.210029e+10 |

| 2017-08-26 | 6.879348e+08 | 4360.5133 | 7.067509e+10 |

| 2017-08-27 | 7.814597e+08 | 4354.3083 | 7.196991e+10 |

| 2017-08-28 | 9.251545e+08 | 4339.0500 | 7.259458e+10 |

| 2017-08-29 | 1.113344e+09 | 4607.9854 | 7.593083e+10 |

| 2017-08-30 | 1.010876e+09 | 4594.9879 | 7.597359e+10 |

| 2017-08-31 | 1.192190e+09 | 4582.5200 | 7.851738e+10 |

# By month's number

btc_usd.loc["08/2017"]

| code | ETRVU | MKPRU | MKTCP |

|---|---|---|---|

| date | |||

| 2017-08-01 | 1.369196e+09 | 2862.9000 | 4.550093e+10 |

| 2017-08-02 | 1.424506e+09 | 2693.6340 | 4.440385e+10 |

| 2017-08-03 | 9.709563e+08 | 2794.1177 | 4.606512e+10 |

| 2017-08-04 | 1.196485e+09 | 2790.0000 | 4.631086e+10 |

| 2017-08-05 | 9.791541e+08 | 3218.1150 | 5.306965e+10 |

| 2017-08-06 | 1.044204e+09 | 3252.5625 | 5.364342e+10 |

| 2017-08-07 | 1.385571e+09 | 3210.2000 | 5.319216e+10 |

| 2017-08-08 | 1.230026e+09 | 3457.3743 | 5.703501e+10 |

| 2017-08-09 | 8.071196e+08 | 3357.3263 | 5.526816e+10 |

| 2017-08-10 | 9.631284e+08 | 3340.2800 | 5.650275e+10 |

| 2017-08-11 | 9.856015e+08 | 3632.5067 | 5.994299e+10 |

| 2017-08-12 | 8.706294e+08 | 3852.8029 | 6.358478e+10 |

| 2017-08-13 | 9.264450e+08 | 3868.5200 | 6.693611e+10 |

| 2017-08-14 | 8.666749e+08 | 4282.9920 | 7.069930e+10 |

| 2017-08-15 | 1.206088e+09 | 4217.0283 | 6.961845e+10 |

| 2017-08-16 | 9.825228e+08 | 4179.9700 | 6.764231e+10 |

| 2017-08-17 | 1.362841e+09 | 4328.7257 | 7.147917e+10 |

| 2017-08-18 | 1.137242e+09 | 4130.4401 | 6.821262e+10 |

| 2017-08-19 | 1.323689e+09 | 4104.7100 | 6.812422e+10 |

| 2017-08-20 | 7.589911e+08 | 4157.9580 | 6.868167e+10 |

| 2017-08-21 | 8.194572e+08 | 4043.7220 | 6.680052e+10 |

| 2017-08-22 | 8.814776e+08 | 3986.2800 | 6.755553e+10 |

| 2017-08-23 | 1.053264e+09 | 4174.9500 | 6.898129e+10 |

| 2017-08-24 | 7.560436e+08 | 4340.3167 | 7.171907e+10 |

| 2017-08-25 | 7.651743e+08 | 4331.7700 | 7.210029e+10 |

| 2017-08-26 | 6.879348e+08 | 4360.5133 | 7.067509e+10 |

| 2017-08-27 | 7.814597e+08 | 4354.3083 | 7.196991e+10 |

| 2017-08-28 | 9.251545e+08 | 4339.0500 | 7.259458e+10 |

| 2017-08-29 | 1.113344e+09 | 4607.9854 | 7.593083e+10 |

| 2017-08-30 | 1.010876e+09 | 4594.9879 | 7.597359e+10 |

| 2017-08-31 | 1.192190e+09 | 4582.5200 | 7.851738e+10 |

Or even a day…

# By date name

btc_usd.loc["August 1, 2017"]

code

ETRVU 1.369196e+09

MKPRU 2.862900e+03

MKTCP 4.550093e+10

Name: 2017-08-01 00:00:00, dtype: float64

# By date number

btc_usd.loc["08-01-2017"]

code

ETRVU 1.369196e+09

MKPRU 2.862900e+03

MKTCP 4.550093e+10

Name: 2017-08-01 00:00:00, dtype: float64

What can we pass as the .loc argument when we have a

DateTimeIndex?

Anything that can be converted to a datetime using

pd.to_datetime, without having to specify the format argument.

When that condition holds, pandas will return all rows whose date in the index “belong” to that date or period.

We can also use the range shorthand notation to give a start and end date for selection.

btc_usd.loc["April 1, 2015":"April 10, 2015"]

| code | ETRVU | MKPRU | MKTCP |

|---|---|---|---|

| date | |||

| 2015-04-01 | 5.354486e+07 | 252.44 | 3.536773e+09 |

| 2015-04-02 | 4.016409e+07 | 246.49 | 3.565053e+09 |

| 2015-04-03 | 4.331351e+07 | 253.77 | 3.549561e+09 |

| 2015-04-04 | 2.205524e+07 | 257.03 | 3.604010e+09 |

| 2015-04-05 | 2.832354e+07 | 253.67 | 3.572161e+09 |

| 2015-04-06 | 3.991755e+07 | 255.48 | 3.584116e+09 |

| 2015-04-07 | 5.134161e+07 | 245.89 | 3.579212e+09 |

| 2015-04-08 | 5.092222e+07 | 253.90 | 3.438417e+09 |

| 2015-04-09 | 5.215728e+07 | 235.71 | 3.309144e+09 |

| 2015-04-10 | 4.316281e+07 | 236.70 | 3.411246e+09 |

Exercise

See exercise 3 in the exercise list.

Accessing Date Properties#

Sometimes, we would like to directly access a part of the date/time.

If our date/time information is in the index, we can to df.index.XX

where XX is replaced by year, month, or whatever we would

like to access.

btc_usd.index.year

Index([2009, 2009, 2009, 2009, 2009, 2009, 2009, 2010, 2010, 2010,

...

2018, 2018, 2018, 2018, 2018, 2018, 2018, 2018, 2018, 2019],

dtype='int32', name='date', length=3295)

btc_usd.index.day

Index([25, 26, 27, 28, 29, 30, 31, 1, 2, 3,

...

23, 24, 25, 26, 27, 28, 29, 30, 31, 1],

dtype='int32', name='date', length=3295)

We can also do the same if the date/time information is stored in a column, but we have to use a slightly different syntax.

df["column_name"].dt.XX

btc_date_column = btc_usd.reset_index()

btc_date_column.head()

| code | date | ETRVU | MKPRU | MKTCP |

|---|---|---|---|---|

| 0 | 2009-12-25 | 0.0 | 0.0 | 0.0 |

| 1 | 2009-12-26 | 0.0 | 0.0 | 0.0 |

| 2 | 2009-12-27 | 0.0 | 0.0 | 0.0 |

| 3 | 2009-12-28 | 0.0 | 0.0 | 0.0 |

| 4 | 2009-12-29 | 0.0 | 0.0 | 0.0 |

btc_date_column["date"].dt.year.head()

0 2009

1 2009

2 2009

3 2009

4 2009

Name: date, dtype: int32

btc_date_column["date"].dt.month.head()

0 12

1 12

2 12

3 12

4 12

Name: date, dtype: int32

Leads and Lags: df.shift#

When doing time series analysis, we often want to compare data at one date against data at another date.

pandas can help us with this if we leverage the shift method.

Without any additional arguments, shift() will move all data

forward one period, filling the first row with missing data.

# so we can see the result of shift clearly

btc_usd.head()

| code | ETRVU | MKPRU | MKTCP |

|---|---|---|---|

| date | |||

| 2009-12-25 | 0.0 | 0.0 | 0.0 |

| 2009-12-26 | 0.0 | 0.0 | 0.0 |

| 2009-12-27 | 0.0 | 0.0 | 0.0 |

| 2009-12-28 | 0.0 | 0.0 | 0.0 |

| 2009-12-29 | 0.0 | 0.0 | 0.0 |

btc_usd.shift().head()

| code | ETRVU | MKPRU | MKTCP |

|---|---|---|---|

| date | |||

| 2009-12-25 | NaN | NaN | NaN |

| 2009-12-26 | 0.0 | 0.0 | 0.0 |

| 2009-12-27 | 0.0 | 0.0 | 0.0 |

| 2009-12-28 | 0.0 | 0.0 | 0.0 |

| 2009-12-29 | 0.0 | 0.0 | 0.0 |

We can use this to compute the percent change from one day to the next. (Quiz: Why does that work? Remember how pandas uses the index to align data.)

((btc_usd - btc_usd.shift()) / btc_usd.shift()).head()

| code | ETRVU | MKPRU | MKTCP |

|---|---|---|---|

| date | |||

| 2009-12-25 | NaN | NaN | NaN |

| 2009-12-26 | NaN | NaN | NaN |

| 2009-12-27 | NaN | NaN | NaN |

| 2009-12-28 | NaN | NaN | NaN |

| 2009-12-29 | NaN | NaN | NaN |

Setting the first argument to n tells pandas to shift the data down

n rows (apply an n period lag).

btc_usd.shift(3).head()

| code | ETRVU | MKPRU | MKTCP |

|---|---|---|---|

| date | |||

| 2009-12-25 | NaN | NaN | NaN |

| 2009-12-26 | NaN | NaN | NaN |

| 2009-12-27 | NaN | NaN | NaN |

| 2009-12-28 | 0.0 | 0.0 | 0.0 |

| 2009-12-29 | 0.0 | 0.0 | 0.0 |

A negative value will shift the data up or apply a lead.

btc_usd.shift(-2).head()

| code | ETRVU | MKPRU | MKTCP |

|---|---|---|---|

| date | |||

| 2009-12-25 | 0.0 | 0.0 | 0.0 |

| 2009-12-26 | 0.0 | 0.0 | 0.0 |

| 2009-12-27 | 0.0 | 0.0 | 0.0 |

| 2009-12-28 | 0.0 | 0.0 | 0.0 |

| 2009-12-29 | 0.0 | 0.0 | 0.0 |

btc_usd.shift(-2).tail()

| code | ETRVU | MKPRU | MKTCP |

|---|---|---|---|

| date | |||

| 2018-12-28 | 2.700024e+08 | 3770.3600 | 6.689905e+10 |

| 2018-12-29 | 4.760031e+08 | 3791.5458 | 6.638886e+10 |

| 2018-12-30 | 2.236265e+08 | 3752.2717 | 6.550566e+10 |

| 2018-12-31 | NaN | NaN | NaN |

| 2019-01-01 | NaN | NaN | NaN |

Exercise

See exercise 4 in the exercise list.

Rolling Computations: .rolling#

pandas has facilities that enable easy computation of rolling statistics.

These are best understood by example, so we will dive right in.

# first take only the first 6 rows so we can easily see what is going on

btc_small = btc_usd.head(6)

btc_small

| code | ETRVU | MKPRU | MKTCP |

|---|---|---|---|

| date | |||

| 2009-12-25 | 0.0 | 0.0 | 0.0 |

| 2009-12-26 | 0.0 | 0.0 | 0.0 |

| 2009-12-27 | 0.0 | 0.0 | 0.0 |

| 2009-12-28 | 0.0 | 0.0 | 0.0 |

| 2009-12-29 | 0.0 | 0.0 | 0.0 |

| 2009-12-30 | 0.0 | 0.0 | 0.0 |

Below, we compute the 2 day moving average (for all columns).

btc_small.rolling("2d").mean()

| code | ETRVU | MKPRU | MKTCP |

|---|---|---|---|

| date | |||

| 2009-12-25 | 0.0 | 0.0 | 0.0 |

| 2009-12-26 | 0.0 | 0.0 | 0.0 |

| 2009-12-27 | 0.0 | 0.0 | 0.0 |

| 2009-12-28 | 0.0 | 0.0 | 0.0 |

| 2009-12-29 | 0.0 | 0.0 | 0.0 |

| 2009-12-30 | 0.0 | 0.0 | 0.0 |

To do this operation, pandas starts at each row (date) then looks

backwards the specified number of periods (here 2 days) and then

applies some aggregation function (mean) on all the data in that

window.

If pandas cannot look back the full length of the window (e.g. when working on the first row), it fills as much of the window as possible and then does the operation. Notice that the value at 2014-05-01 is the same in both DataFrames.

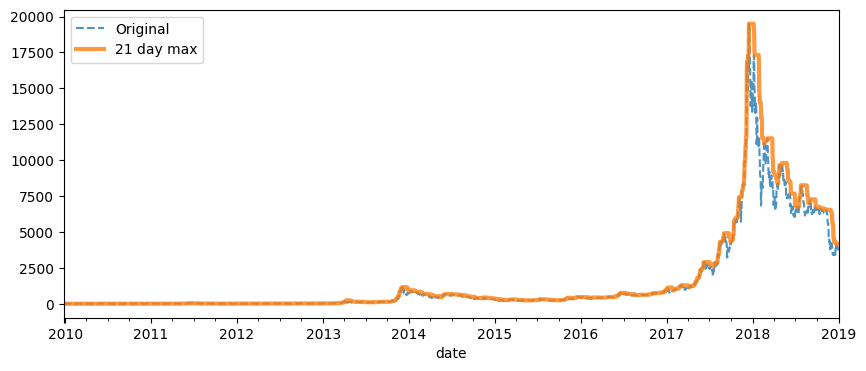

Below, we see a visual depiction of the rolling maximum on a 21 day window for the whole dataset.

fig, ax = plt.subplots(figsize=(10, 4))

btc_usd["MKPRU"].plot(ax=ax, linestyle="--", alpha=0.8)

btc_usd.rolling("21d").max()["MKPRU"].plot(ax=ax, alpha=0.8, linewidth=3)

ax.legend(["Original", "21 day max"])

<matplotlib.legend.Legend at 0x7fe232d81ac0>

We can also ask pandas to apply custom functions, similar to what we

saw when studying GroupBy.

def is_volatile(x):

"Returns a 1 if the variance is greater than 1, otherwise returns 0"

if x.var() > 1.0:

return 1.0

else:

return 0.0

btc_small.rolling("2d").apply(is_volatile)

| code | ETRVU | MKPRU | MKTCP |

|---|---|---|---|

| date | |||

| 2009-12-25 | 0.0 | 0.0 | 0.0 |

| 2009-12-26 | 0.0 | 0.0 | 0.0 |

| 2009-12-27 | 0.0 | 0.0 | 0.0 |

| 2009-12-28 | 0.0 | 0.0 | 0.0 |

| 2009-12-29 | 0.0 | 0.0 | 0.0 |

| 2009-12-30 | 0.0 | 0.0 | 0.0 |

Exercise

See exercise 5 in the exercise list.

To make the optimal decision, we need to know the maximum difference between the close price at the end of the window and the open price at the start of the window.

Exercise

See exercise 6 in the exercise list.

Changing Frequencies: .resample#

In addition to computing rolling statistics, we can also change the frequency of the data.

For example, instead of a monthly moving average, suppose that we wanted to compute the average within each calendar month.

We will use the resample method to do this.

Below are some examples.

# business quarter

btc_usd.resample("BQE").mean()

| code | ETRVU | MKPRU | MKTCP |

|---|---|---|---|

| date | |||

| 2009-12-31 | 0.000000e+00 | 0.000000 | 0.000000e+00 |

| 2010-03-31 | 0.000000e+00 | 0.000000 | 0.000000e+00 |

| 2010-06-30 | 0.000000e+00 | 0.000000 | 0.000000e+00 |

| 2010-09-30 | 8.522276e+02 | 0.033260 | 1.317223e+05 |

| 2010-12-31 | 1.179063e+04 | 0.217938 | 1.015812e+06 |

| 2011-03-31 | 4.516475e+04 | 0.737402 | 4.043357e+06 |

| 2011-06-30 | 1.729951e+06 | 9.176310 | 5.956523e+07 |

| 2011-09-30 | 9.176091e+05 | 10.742849 | 7.522893e+07 |

| 2011-12-30 | 1.991838e+06 | 3.419525 | 2.639635e+07 |

| 2012-03-30 | 7.588531e+05 | 5.592202 | 4.670274e+07 |

| 2012-06-29 | 1.101213e+06 | 5.407497 | 4.886157e+07 |

| 2012-09-28 | 2.821250e+06 | 10.356359 | 1.007798e+08 |

| 2012-12-31 | 2.701674e+06 | 12.368074 | 1.286258e+08 |

| 2013-03-29 | 8.611094e+06 | 32.621256 | 3.515062e+08 |

| 2013-06-28 | 2.782766e+07 | 119.419551 | 1.337195e+09 |

| 2013-09-30 | 1.979282e+07 | 107.674014 | 1.242022e+09 |

| 2013-12-31 | 1.081436e+08 | 494.289457 | 6.009161e+09 |

| 2014-03-31 | 9.001297e+07 | 693.245444 | 8.591035e+09 |

| 2014-06-30 | 5.479866e+07 | 520.799451 | 6.665094e+09 |

| 2014-09-30 | 5.296835e+07 | 534.162283 | 7.020311e+09 |

| 2014-12-31 | 6.272862e+07 | 357.784674 | 4.835176e+09 |

| 2015-03-31 | 5.113746e+07 | 250.173111 | 3.481522e+09 |

| 2015-06-30 | 4.752748e+07 | 236.218681 | 3.355567e+09 |

| 2015-09-30 | 6.545561e+07 | 255.963913 | 3.712326e+09 |

| 2015-12-31 | 1.385931e+08 | 345.638152 | 5.142968e+09 |

| 2016-03-31 | 1.283647e+08 | 409.983516 | 6.226075e+09 |

| 2016-06-30 | 1.665296e+08 | 510.586051 | 7.972975e+09 |

| 2016-09-30 | 1.499507e+08 | 615.694674 | 9.752593e+09 |

| 2016-12-30 | 1.928515e+08 | 724.429451 | 1.163821e+10 |

| 2017-03-31 | 2.747348e+08 | 1033.310616 | 1.667005e+10 |

| 2017-06-30 | 5.764680e+08 | 1900.426105 | 3.122785e+10 |

| 2017-09-29 | 8.735033e+08 | 3461.377390 | 5.764089e+10 |

| 2017-12-29 | 2.332756e+09 | 9258.879054 | 1.552192e+11 |

| 2018-03-30 | 1.906414e+09 | 10664.432624 | 1.792487e+11 |

| 2018-06-29 | 9.201284e+08 | 7787.273765 | 1.320632e+11 |

| 2018-09-28 | 7.135467e+08 | 6797.888576 | 1.170264e+11 |

| 2018-12-31 | 7.343926e+08 | 5248.198650 | 9.075620e+10 |

| 2019-03-29 | 2.236265e+08 | 3752.271700 | 6.550566e+10 |

Note that unlike with rolling, a single number is returned for

each column for each quarter.

The resample method will alter the frequency of the data and the

number of rows in the result will be different from the number of rows

in the input.

On the other hand, with rolling, the size and frequency of the result

are the same as the input.

We can sample at other frequencies and aggregate with multiple aggregations function at once.

# multiple functions at 2 start-of-quarter frequency

btc_usd.resample("2BQS").agg(["min", "max"])

| code | ETRVU | MKPRU | MKTCP | |||

|---|---|---|---|---|---|---|

| min | max | min | max | min | max | |

| date | ||||||

| 2009-10-01 | 0.000000e+00 | 0.000000e+00 | 0.0000 | 0.0000 | 0.000000e+00 | 0.000000e+00 |

| 2010-04-01 | 0.000000e+00 | 4.780000e+03 | 0.0000 | 0.1750 | 0.000000e+00 | 6.992825e+05 |

| 2010-10-01 | 1.649000e+03 | 2.441970e+05 | 0.0600 | 1.1000 | 2.493210e+05 | 5.901940e+06 |

| 2011-04-01 | 2.740300e+04 | 1.815384e+07 | 0.7100 | 35.0000 | 4.150234e+06 | 2.272585e+08 |

| 2011-10-03 | 1.975250e+05 | 1.637516e+07 | 2.2900 | 7.2200 | 1.766128e+07 | 5.811768e+07 |

| 2012-04-02 | 4.122260e+05 | 1.322970e+07 | 4.8000 | 15.4000 | 4.195824e+07 | 1.496572e+08 |

| 2012-10-01 | 7.742860e+05 | 2.769433e+07 | 10.6010 | 93.5670 | 1.093527e+08 | 1.125488e+09 |

| 2013-04-01 | 9.821585e+06 | 1.385370e+08 | 67.8584 | 237.9900 | 7.519925e+08 | 2.620841e+09 |

| 2013-10-01 | 1.150644e+07 | 3.843574e+08 | 103.8500 | 1151.0000 | 1.230957e+09 | 1.350490e+10 |

| 2014-04-01 | 1.976148e+07 | 1.765106e+08 | 380.0000 | 673.9000 | 4.661392e+09 | 8.668279e+09 |

| 2014-10-01 | 2.502690e+07 | 1.781682e+08 | 176.5000 | 430.0700 | 2.707305e+09 | 5.802913e+09 |

| 2015-04-01 | 2.205524e+07 | 1.056422e+08 | 216.0000 | 310.5500 | 3.077795e+09 | 4.464575e+09 |

| 2015-10-01 | 4.002130e+07 | 3.353970e+08 | 237.7800 | 463.9800 | 3.486830e+09 | 6.952138e+09 |

| 2016-04-01 | 7.246670e+07 | 4.338279e+08 | 416.2500 | 754.3600 | 6.402758e+09 | 1.212991e+10 |

| 2016-10-03 | 1.006182e+08 | 5.526767e+08 | 607.1800 | 1287.0000 | 9.676305e+09 | 2.089075e+10 |

| 2017-04-03 | 1.955462e+08 | 1.772644e+09 | 1079.9900 | 4911.7400 | 1.846992e+10 | 7.969529e+10 |

| 2017-10-02 | 5.506455e+08 | 5.729890e+09 | 4225.1750 | 19498.6833 | 7.021588e+10 | 3.346692e+11 |

| 2018-04-02 | 2.724822e+08 | 1.986371e+09 | 5908.7025 | 9803.3067 | 1.005508e+11 | 1.668274e+11 |

| 2018-10-01 | 2.236265e+08 | 2.721201e+09 | 3242.4200 | 6626.8500 | 5.620096e+10 | 1.146456e+11 |

As with groupby and rolling, you can also provide custom

functions to .resample(...).agg and .resample(...).apply

Exercise

See exercise 7 in the exercise list.

To make the optimal decision we need to, for each month, compute the maximum value of the close price on any day minus the open price on the first day of the month.

Exercise

See exercise 8 in the exercise list.

Optional: API keys#

Recall above that we had the line of code:

ndl.ApiConfig.api_key = os.environ.get("NASDAQ_DATA_LINK_API_KEY", "jEKP58z7JaX6utPkkpEp")

This line told the nasdaqdatalink library that when obtaining making requests for data, it should use the API key jEKP58z7JaX6utPkkpEp.

An API key is a sort of password that web services (like the Nasdaq Data Link API) require you to provide when you make requests.

Using this password, we were able to make a request to Nasdaq data link to obtain data directly from them.

The API key used here is one that we requested on behalf of this course. If you create your own API key, you should store it in the NASDAQ_DATA_LINK_API_KEY environment variable, locally on your computer. Using an environment variable like this is a common way to store sensitive information like API keys, since you can set the environment variable in a secure way that is not stored in your code. How to set environment variables varies by operating system, but you can find instructions for doing so on the web.

If you plan to use Nasdaq data more extensively, you should obtain your own personal API key from their website and re-run the os.environ... line of code with your new API key on the right-hand side.

Exercises#

Exercise 1#

By referring to table found at the link above, figure out the correct argument to

pass as format in order to parse the dates in the next three cells below.

Test your work by passing your format string to pd.to_datetime.

christmas_str2 = "2017:12:25"

dbacks_win = "M:11 D:4 Y:2001 9:15 PM"

america_bday = "America was born on July 4, 1776"

Exercise 2#

Use pd.to_datetime to express the birthday of one of your friends

or family members as a datetime object.

Then use the strftime method to write a message of the format:

NAME's birthday is June 10, 1989 (a Saturday)

(where the name and date are replaced by the appropriate values)

Exercise 3#

For each item in the list, extract the specified data from btc_usd:

July 2017 through August 2017 (inclusive)

April 25, 2015 to June 10, 2016

October 31, 2017

Exercise 4#

Using the shift function, determine the week with the largest percent change

in the volume of trades (the "Volume (BTC)" column).

Repeat the analysis at the bi-weekly and monthly frequencies.

Hint

We have data at a daily frequency and one week is 7 days.

Hint

Approximate a month by 30 days.

# your code here

Exercise 5#

Imagine that you have access to the DeLorean time machine from “Back to the Future”.

You are allowed to use the DeLorean only once, subject to the following conditions:

You may travel back to any day in the past.

On that day, you may purchase one bitcoin at market open.

You can then take the time machine 30 days into the future and sell your bitcoin at market close.

Then you return to the present, pocketing the profits.

How would you pick the day?

Think carefully about what you would need to compute to make the optimal choice. Try writing it out in the markdown cell below so you have a clear description of the want operator that we will apply after the exercise.

(Note: Don’t look too far below, because in the next non-empty cell we have written out our answer.)

To make this decision, we want to know …

Your answer here

Exercise 6#

Do the following:

Write a pandas function that implements your strategy.

Pass it to the

aggmethod ofrolling_btc.Extract the

"Open"column from the result.Find the date associated with the maximum value in that column.

How much money did you make? Compare with your neighbor.

def daily_value(df):

# DELETE `pass` below and replace it with your code

pass

rolling_btc = btc_usd.rolling("30d")

# do steps 2-4 here

Exercise 7#

Now suppose you still have access to the DeLorean, but the conditions are slightly different.

You may now:

Travel back to the first day of any month in the past.

On that day, you may purchase one bitcoin at market open.

You can then travel to any day in that month and sell the bitcoin at market close.

Then return to the present, pocketing the profits.

To which month would you travel? On which day of that month would you return to sell the bitcoin?

Discuss with your neighbor what you would need to compute to make the optimal choice. Try writing it out in the markdown cell below so you have a clear description of the want operator that we will apply after the exercise.

(Note: Don’t look too many cells below, because we have written out our answer.)

To make the optimal decision we need …

Your answer here

Exercise 8#

Do the following:

Write a pandas function that implements your strategy.

Pass it to the

aggmethod ofresampled_btc.Extract the

"Open"column from the result.Find the date associated with the maximum value in that column.

How much money did you make? Compare with your neighbor.

Was this strategy more profitable than the previous one? By how much?

def monthly_value(df):

# DELETE `pass` below and replace it with your code

pass

resampled_btc = btc_usd.resample("MS")

# Do steps 2-4 here